Forecasts for the 2023 property market were quite varied. Most forecasters predicted that prices would fall by around 10%, driven by the rapid increase in the Bank Rate causing mortgage rates to rise and payments to pretty much double for those on variable or tracker rates, or coming off fixed rates. At the lower end of the spectrum, Zoopla predicted prices would drop by 5%, while some suggested falls could be as much as 20%. Meanwhile, rental forecasts were more optimistic – around a 3%-4% rise, year on year.

However, the property market doesn’t seem to want to play ball with the forecasters. Some predicted prices would collapse after the Brexit vote in 2016; then following the 2019 election; then it was said that the pandemic would bring prices crashing down - and finally the Truss budget and rapid rise in mortgage rates has led to some predictions of a market crash.

But so far this year, although things have certainly stalled after the last few years of exceptional growth, we are still not seeing a collapse in the buying and selling market, and new lets for landlords are still rising at an unexpectedly high rate.

What does the data show for this year so far?

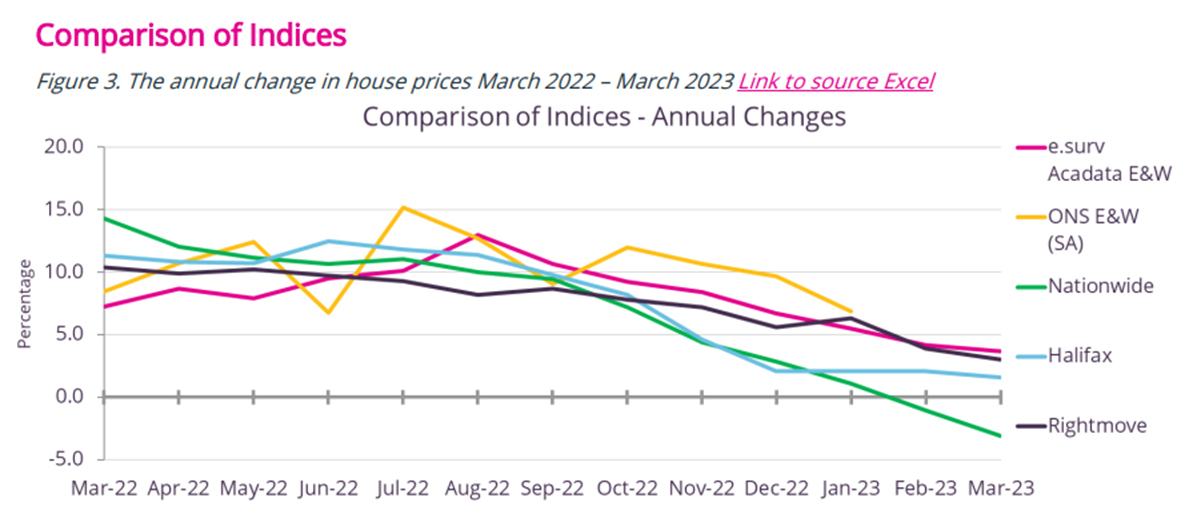

According to most of the indices for England and Wales, including our own e.surv index, property price growth has been falling month on month, but this hasn’t negatively impacted average values, which are still higher than they were at the same time last year. The only index suggesting prices have fallen is Nationwide, but that’s only by a few percent.

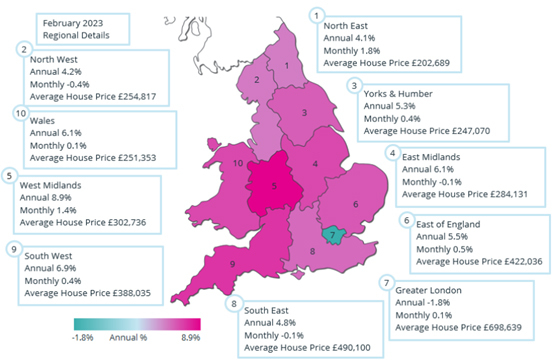

The one area struggling in England from a year-on-year price perspective is Greater London, which is most likely due to the mortgage rises impacting affordability more harshly here than in other regions.

Monthly and annualised regional property price performance

Produced by Acadata on behalf of e.surv

Richard Sexton, director at e.surv, explains: “The key observation is that while price growth is reducing, prices for actual completed transactions are not falling. This points to a continued shortage in the market of the right kind of property for buyers and that affordability concerns, which have been compounded by rising interest rates and the cost-of-living pressures, have been partly offset by the number of lenders competing for business in a market of fewer transactions. There is also evidence that buyers are cutting their cloth in terms of the type of property they expect to purchase.”

As always in property, this data is based on averages and price performance will vary depending on where you live and the type of property you are looking to buy or sell, or own.

Perhaps surprisingly, first-time buyers (FTBs) remain a key driver for sales this year, according to Rightmove and Zoopla, with Rightmove figures suggesting that sales are up by 4% versus March 2019 (which is considered a ‘normal year’, unlike the recent pandemic sales figures). The reason why FTBs are perhaps surviving better than expected is that although mortgage rates have increased, FTBs have been assessed for mortgages at interest rates of around 6% since 2014, so not much has changed for them. And with rents rising rapidly and significant rental stock shortages in many areas, there is a big incentive to buy.

Tied into this, flats are currently selling better than they did during the pandemic, especially in London, according to Zoopla. This is believed to be because the average price of houses has, for most, risen by so much more than flats over the last few years, so Londoners who would normally have moved out of the city to live in a house, are actually finding it’s better value to stay, continue with flat living and avoid the hassle and cost of commuting.

So, depending on where you’re buying or selling, there may be some bargains around this year, or you may find that property prices are holding up much better than expected, which is particularly good news if you’re looking at remortgaging, as an improved loan to value should mean you’re still able to access a reasonable mortgage rate. If you’d like to discuss your options, just get in touch with our partners at Embrace Financial Services for a free initial consultation.

The rental market remains strong

Rents are still rising year on year and, although this growth is expected to slow down, prices continue to perform at a good rate.

According to the government’s own ONS figures, annual private rent rises are at their highest levels since records began. Over the 12 months to March 2023, rental prices increased by:

- 4.6% in England, where the series began in January 2006

- 4.4% in Wales, where the series began in January 2010

- 5.1% in Scotland, where series began in January 2012

But these figures underestimate the rises landlords are securing for new lets, as they include existing tenants, many of whom don’t see their rents increase until they leave the property.

Many landlords are still seeing double-digit rises for new lets, with Zoopla reporting rents rising by 11% in the year to March 2023, due to a continuing excess of tenant demand over the supply of rental properties. Zoopla expects rental growth to continue over this year, reducing to between 4% and 5% by December.

What’s the outlook for landlords?

For any landlord that owned rental properties prior to the pandemic, it’s likely they will have seen good capital growth and, if new tenants have been moved in, good rises in rents too. However, some landlords will be worried about the increase in mortgage interest rates and the new Rent Reform laws we’re expecting to see introduced within the next couple of years, especially the loss of Section 21 to evict a tenant.

Nevertheless, from an investment perspective, property is forecast to continue to deliver positive capital growth returns in the long term, and for those landlords that buy in areas where rental demand is higher than supply, positive income returns are also likely to continue.

However, prices and rents are very individual and can be quite different even from one end of a street to the other. So if you want to know whether you should put your property investments on hold or expand your portfolio, then come and talk to your local Reeds Rains agent and they can help you work out the best next step – for you and your property investment.

Bank of England Base Rate Reaches 4.5%

In its continuing effort to bring inflation under control, the Bank of England increased the base interest rate by 0.25% in May - the 12th rise in 18 months. The good news is this rise was forecast, so it’s likely to be built in to existing mortgage rates, although it will impact on those on tracker rates, so if you’re planning to buy or need to remortgage in the coming months, do speak to a broker who’s experienced in buy to let in plenty of time so you understand what your mortgage payments are likely to be.

Our partners at Embrace Financial Services are always here to help, so if you’d like to find out the latest rates and discuss your mortgage options, you can easily request a callback to book an appointment via our website.

YOUR PROPERTY MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Embrace Financial Services usually charges a fee for mortgage advice. The precise amount of the fee will depend upon your circumstances but will range from £499 to £999 and this will be discussed and agreed with you at the earliest opportunity.

Most Buy-to-Let Mortgages are not regulated by the Financial Conduct Authority’